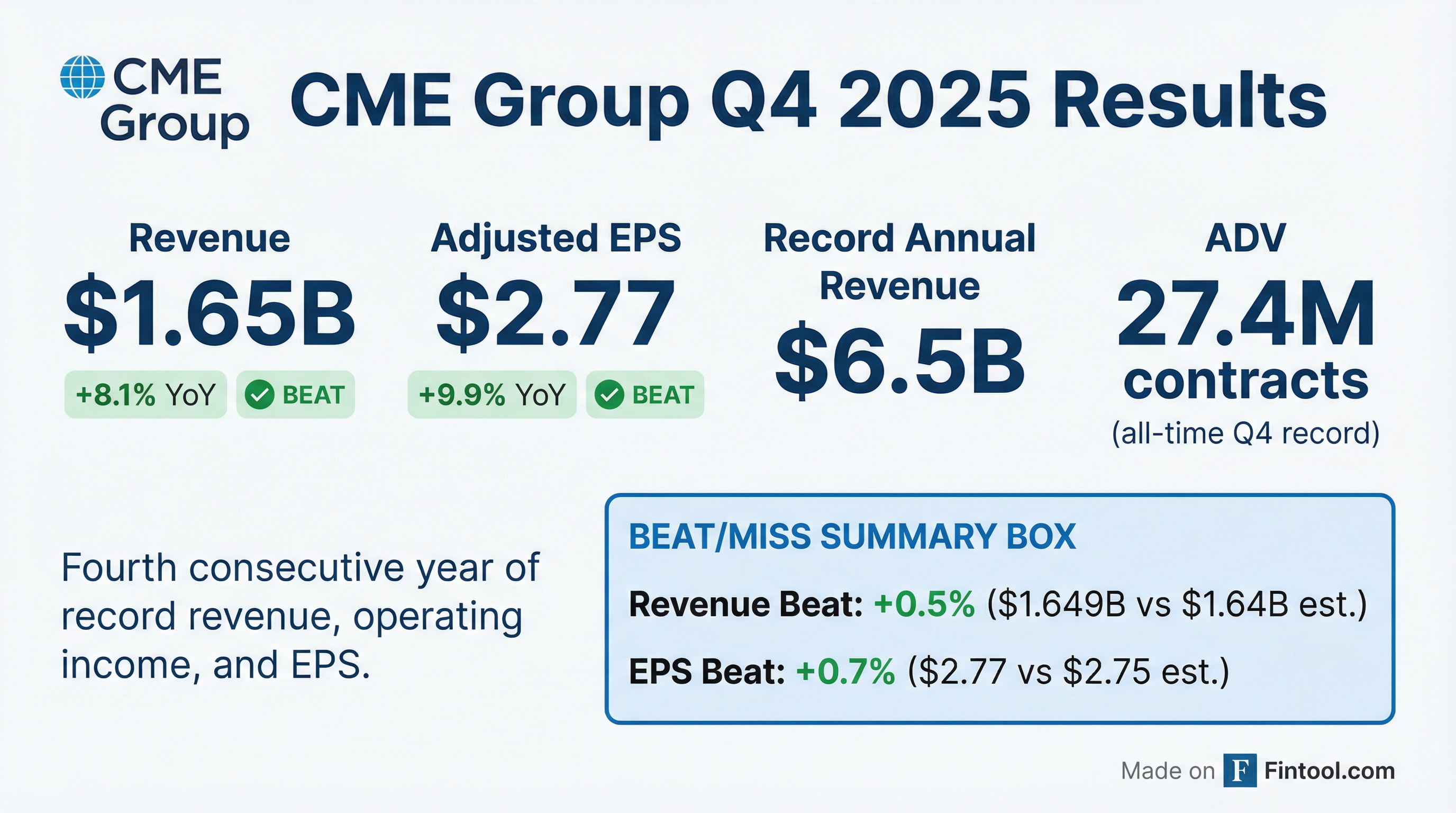

Earnings summaries and quarterly performance for CME GROUP.

Executive leadership at CME GROUP.

Terrence A. Duffy

Chairman and Chief Executive Officer

Derek Sammann

Senior Managing Director, Global Head of Commodities Markets

Hilda Harris Piell

Chief Human Resources Officer

Jack Tobin

Managing Director and Chief Accounting Officer

Jonathan Marcus

Senior Managing Director and General Counsel

Julie Winkler

Chief Commercial Officer

Kendal Vroman

Chief Transformation Officer

Lynne Fitzpatrick

President and Chief Financial Officer

Michael Dennis

Senior Managing Director, Global Head of Fixed Income

Sunil Cutinho

Chief Information Officer

Suzanne Sprague

Chief Operating Officer and Global Head of Clearing

Tim McCourt

Senior Managing Director, Global Head of Equities, FX and Alternate Products

Board of directors at CME GROUP.

Bryan T. Durkin

Director

Charles P. Carey

Director

Daniel G. Kaye

Director

Deborah J. Lucas

Director

Dennis A. Suskind

Lead Independent Director

Elizabeth A. Cook

Director

Harold Ford Jr.

Director

Howard J. Siegel

Director

Kathryn Benesh

Director

Martin J. Gepsman

Director

Patrick J. Mulchrone

Director

Patrick W. Maloney

Director

Phyllis M. Lockett

Director

Rahael Seifu

Director

Robert J. Tierney Jr.

Director

Timothy S. Bitsberger

Director

William R. Shepard

Director

William W. Hobert

Director

Research analysts who have asked questions during CME GROUP earnings calls.

Brian Bedell

Deutsche Bank

9 questions for CME

Michael Cyprys

Morgan Stanley

9 questions for CME

Craig Siegenthaler

Bank of America

8 questions for CME

Patrick Moley

Piper Sandler & Co.

8 questions for CME

Dan Fannon

Jefferies & Company Inc.

6 questions for CME

Kenneth Worthington

JPMorgan Chase & Co.

6 questions for CME

Kyle Voigt

Keefe, Bruyette & Woods

6 questions for CME

Alex Kramm

UBS Group AG

5 questions for CME

Benjamin Budish

Barclays PLC

5 questions for CME

Christopher Allen

Citigroup

5 questions for CME

Simon Clinch

Redburn Atlantic

5 questions for CME

Ben Budish

Barclays PLC

4 questions for CME

William Katz

TD Cowen

4 questions for CME

Alexander Blostein

Goldman Sachs

3 questions for CME

Ashish Sabadra

RBC Capital Markets

3 questions for CME

Daniel Fannon

Jefferies Financial Group Inc.

3 questions for CME

Kwun Sum Lau

Oppenheimer

3 questions for CME

Anthony Valentini

Goldman Sachs

2 questions for CME

Bill Katz

TD Securities

2 questions for CME

Chris Allen

Citi

2 questions for CME

Eli Abboud

Bank of America

2 questions for CME

Ken Worthington

JPMorgan

2 questions for CME

Owen Lau

Oppenheimer & Co. Inc.

2 questions for CME

Will Chi

RBC Capital Markets

2 questions for CME

William Qi

RBC Capital Markets

2 questions for CME

Kyle Voit

KBW

1 question for CME

Simon Alistair Clinch

Redburn Atlantic

1 question for CME

Recent press releases and 8-K filings for CME.

- CME reported 28.1 million average daily volume in 2025 (+6% YoY) and 6% revenue growth, achieving a 69.4% adjusted operating margin; YTD ADV reached 35.5 million (+16%) as of early 2026

- Non-US participation is a key growth driver, with non-US volumes growing ~10% CAGR over five years and 47% of FX and metals ADV originating outside the U.S. in Q4 2025

- Retail expansion via micro contracts—e.g., 1-ounce gold at 35% of the standard contract price—has onboarded new-to-futures traders, generating high-margin volume (45% of retail ADV is non-U.S.)

- Commodities remain core, with $1.8 B in energy, $650 M in agriculture and $350 M in metals revenues, and $80 B/day of cross-margin offsets enhancing customer capital efficiency

- Non-transactional revenues include an $800 M market data business (+13% YoY), SPDJI royalties and $600 M in interest on collateral; CME offers a 4.1% dividend yield (incl. $6.15 annual variable dividend) and has an active share buyback program

- CME Group positions itself as the world’s leading derivatives exchange with a dual mandate of price transparency through benchmark futures and options across six major asset classes and risk management via its vertically integrated clearinghouse.

- In CY 2025, CME achieved 6% ADV growth to 28.1 million contracts/day and 6% revenue growth with a 69.4% adjusted operating margin; year-to-date ADV is 35.5 million, up 16%.

- Non-U.S. volumes are a key growth driver, led by Europe, with non-U.S. business growing at ~10% over five years and higher rate-per-contract margins.

- Retail expansion via the micro contract suite (e.g., Micro Gold, Micro E-mini) is attracting net new customers, with 45% of retail volume now from non-U.S. clients.

- Diversified non-transactional revenues include an $800 m market data business (+13%), income from a 27% S&P Dow Jones Indices stake, and $600 m in interest on collateral, supporting a 4.1% dividend yield, annual variable dividend, and ongoing share buyback.

- CME Group reported 2025 ADV of 28.1 M contracts (+6% YoY) and revenues +6%, with $5.3 B transactional and $1.7 B non-transactional revenue, achieving 69.4% adjusted operating margin; YTD ADV reached 35.5 M (+16%), peaking at 45 M contracts during recent volatility.

- Growth is driven by the non-U.S. client base, with nearly 50% of FX and metals volumes from outside the U.S. and non-U.S. ADV outpacing U.S. at ~10% CAGR over five years, yielding higher rate-per-contract margins.

- CME is expanding its retail footprint via micro-contracts (e.g., 1-ounce gold), capturing new-to-futures traders; this high-margin segment now constitutes ~45% of retail volume outside the U.S..

- The commodities segment delivers ~$1.8 B in energy, $650 M in agriculture, and $350 M in metals, and leverages $80 B/day in cross-margin offsets to enhance capital efficiency and client stickiness.

- CME Group achieved a record 37.6 million average daily volume (ADV) in February, 14% higher year-over-year.

- Interest Rate ADV hit 21.3 million contracts, including a record 13.7 million U.S. Treasury futures and options ADV.

- Equity Index ADV reached 8.4 million, Energy ADV was 3.2 million, and Agricultural ADV was 2.3 million contracts in February.

- International ADV set a record 11.6 million contracts, with EMEA at 8.7 million and APAC ADV up 16% to 2.4 million.

- CME Group’s U.S. Treasury futures and options open interest (OI) hit a record 36,328,151 contracts on February 19, 2026, surpassing the prior high of 35,120,066 set in November 2025

- Key product records include 5.8 million 2-Year note contracts, 7.9 million 5-Year note contracts, 12.6 million 10-Year note contracts, and 3.6 million 30-Year bond contracts

- A record 2,100 large open interest holders were reported in the CFTC’s February 10 Commitment of Traders report

- CME Group noted over $25 billion in daily margin savings and portfolio/cross-margining benefits for its U.S. Treasury and SOFR futures

- CME Group will offer 24/7 continuous trading for Bitcoin- and Ethereum-linked futures and options on CME Globex starting May 29, pending regulatory approval, with a two-hour weekly maintenance window.

- The move responds to record client demand—about $3 trillion in notional crypto volume in 2025 and a 46% Y/Y rise in average daily crypto volume to ~407,200 contracts, with open interest near 335,400.

- Weekend trades will carry the next business day’s trade date, while clearing, settlement and regulatory reporting will follow traditional post-trade processes.

- Aimed at closing timing gaps for institutional hedging between regulated derivatives and spot markets, the plan has CFTC chair Mike Selig’s support but still requires regulatory sign-off.

- CME Group will offer 24/7 trading of regulated cryptocurrency futures and options starting May 29, pending regulatory approval.

- In 2025, its cryptocurrency futures and options reached a record $3 trillion in notional volume, reflecting robust client demand.

- Year-to-date 2026 highlights include average daily volume of 407,200 contracts (+46% YoY), average daily open interest of 335,400 contracts (+7% YoY) and futures ADV of 403,900 contracts (+47% YoY).

- CME Group declares an annual variable dividend of $6.15 per share, totaling approximately $2.2 billion, based on 2025 results, payable March 26, 2026, to shareholders of record March 10, 2026.

- The Q1 2026 regular dividend is set at $1.30 per share, a $0.05 increase from the prior level.

- Combined with quarterly dividends paid during 2025, total annual payouts reach $4.0 billion, representing a 4.2% total dividend yield based on the average 2025 closing stock price.

- CME Group plans to introduce four cash-settled South Asia edible oil futures contracts on March 2, 2026, pending regulatory approval, covering soybean oil, crude palm oil and two spread products.

- The contracts use Fastmarkets Soyoil CFR India and Crude Palm Oil CFR West Coast India indices to enhance price discovery and risk management in South Asia, which accounts for approximately 45% of soyoil and 30% of palm oil trade globally.

- In 2025, CME Group achieved record agricultural average daily volume of 1.9 million contracts, including 293,000 soybean futures and 182,000 soybean oil futures contracts.

- The new products will be listed on CBOT under its rules, offering additional hedging tools for edible oil price exposure.

- CME Group launched Cardano (ADA), Chainlink (LINK) and Stellar (XLM) futures on February 9, 2026, expanding its regulated cryptocurrency product suite.

- The first LINK and XLM futures trades were executed between FalconX and Marex, while the inaugural ADA futures trade occurred between Cumberland DRW and Wintermute.

- These contracts are available in micro- and larger-sized formats, offering capital-efficient tools for institutional price risk management.

- CME Group stated the launch reflects growing client demand for trusted, regulated crypto derivatives.

Fintool News

In-depth analysis and coverage of CME GROUP.

CME Group Goes 24/7: World's Largest Derivatives Exchange Brings Always-On Trading to Crypto Futures

CME Crypto Derivatives Hit Record $12 Billion Daily Volume as Institutional Adoption Accelerates

The Prediction Markets War Heats Up: FanDuel, DraftKings, and Coinbase Race for $100B Market

Quarterly earnings call transcripts for CME GROUP.

Ask Fintool AI Agent

Get instant answers from SEC filings, earnings calls & more